We're now moving onto the cash flow statement. A problem faced in assessing companies is that they can be profitable but lack cash flow. Sales can be recorded but the cash only comes in after period of delay as suppliers sometimes gives customers generous credit terms. The cash flow statement is, thus, a very recent development, made compulsory in the US in 1988.

There are three main components to the cash flow statement :

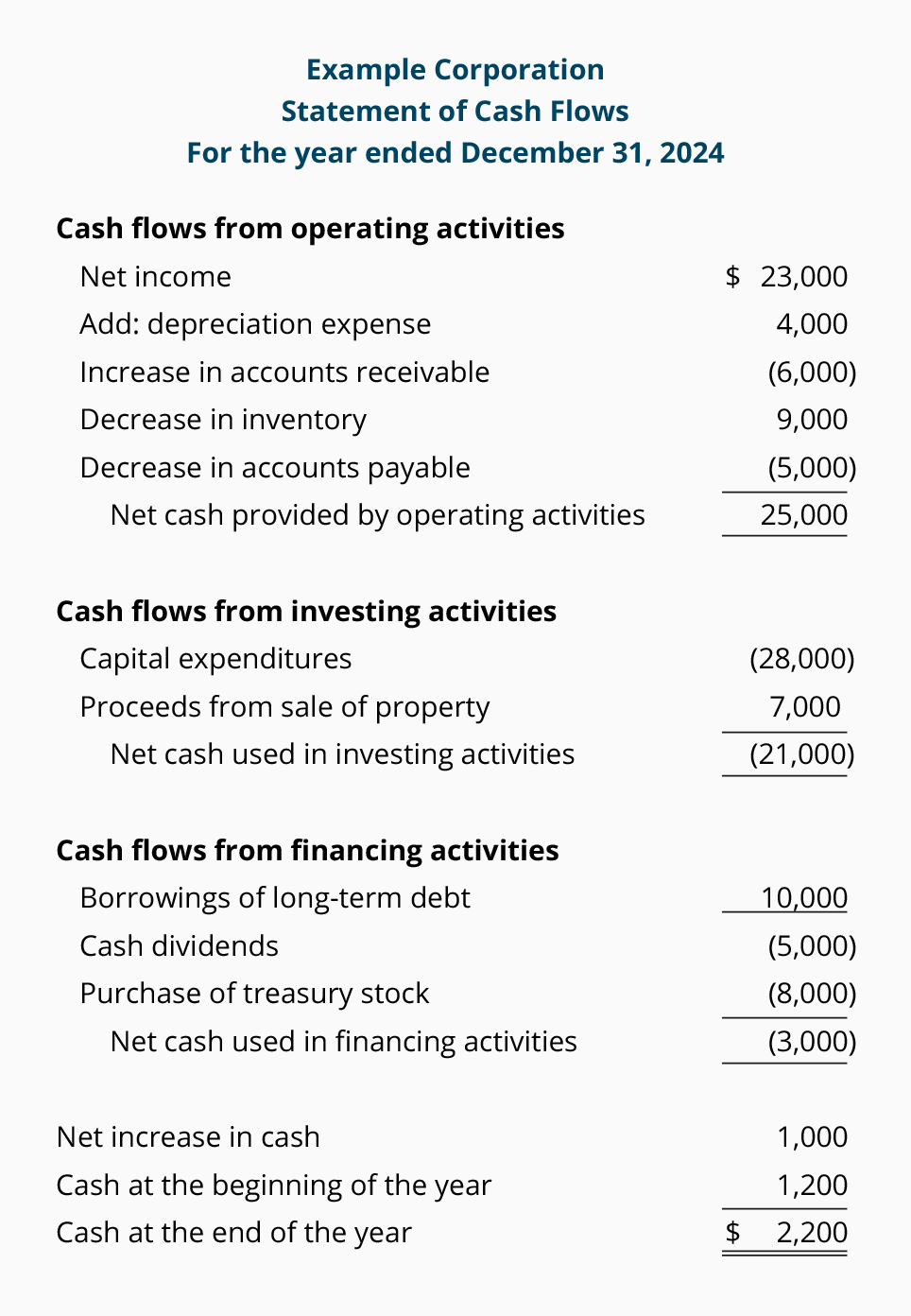

a) Cash flow from Operating Activities

Measures cash obtained from direct business operations like selling of goods or services. When cash owed is paid to the business by a customer, it is recorded here.

b) Cash flow from investing activities

When you buy plant and equipment, you record the outgoing cash flow here. Companies that sell their means of production will have to record proceeds here. If dividends come from selling plant equipment, this should raise an alarm bell.

c) Cash flow from financing activities

When you get a bank loan or issue shares, the cash flow can be found here. Dividends paid are also found in this section of the cash flow statement.

The cash flow statement is an enabler for dividends investors. When we wish to see whether dividends are sustainable, we normally calculate the ( Cash Flow from Operations - Capital Expenditure ). If this number is higher than dividends given out, we have some assurance that dividends are sustainable moving forward.

Consequently, when back-testing Singapore dividend stocks over the past 10 years, companies that have sustainable dividends have a much improved performance.

No comments:

Post a Comment