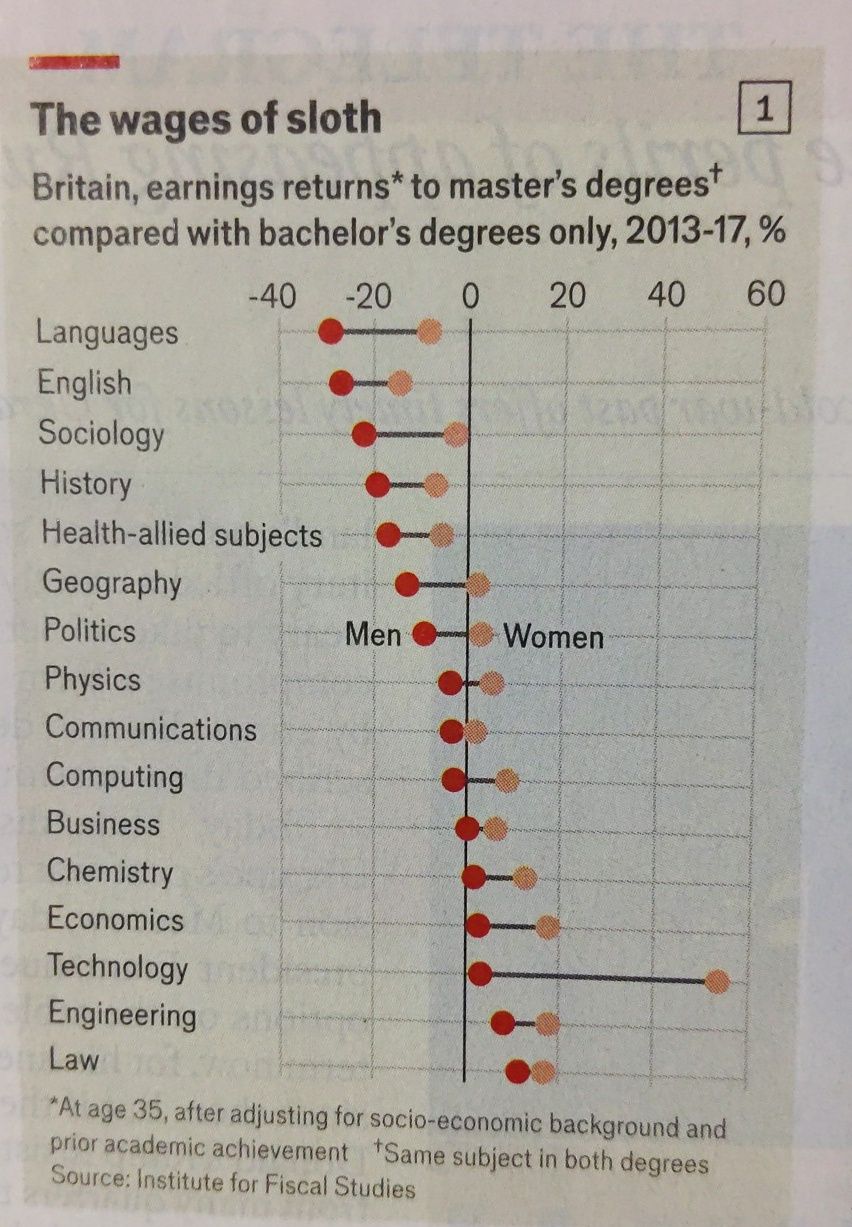

About 3 weeks ago, The Economist published some earnings returns to folks with Master's degrees and measured the value added of these qualifications over those with bachelor's degrees. They found that after adjusting for social and economic status and previous job roles, these degrees do not add much value to the person taking it.

But the actual data is a lot more damning - folks who had advanced degrees in languages, sociology, English and history actually earned significantly less than those who only had bachelor's degrees, which sort of makes you wonder what kind of folks peddle these programs. If your only career recourse after studying for an advanced degree is to teach the same subject in another institution, then you are no different from someone who sells MLM. You might be part of a humanities Pyramid scheme.

Naturally, the response to the Economist was quick and aggressive, with many academics writing articles to defend their product and saying things like an ROI should not be the primary reason why people should spend more time in school. Ideally, people should be driven by their love for learning. Of course, none of them addressed the elephant in the room - if you have a Master's degree in English or Languages, it would destroy more than 20% of your earning returns!

Another critical data point is why women benefit much more from a Master's degree. The Economist explains that advanced degrees mitigate the motherhood penalty, and women with these degrees continue to pour a lot of work into their careers. Sadly, no troll jumped on this point - men who are about to date highly qualified women need to be put on notice that they will commit less to their families. It's a valid conclusion as well that the manosphere should jump on!

Of course, MBAs are right in the middle of the pack; in the Economist article, MBAs generally do not add any value, but the article hints that very prestigious MBAs tend to have high ROIs. And I'm happy that the Business Times today had an excellent article to fill out the gaps for MBA programs.

The numbers reflect well for the MBA programs - yes, even those for NUS and SMU which are not precisely programs you attend for a higher income, but something you need to have an alternative other than the public sector. When I was studying for my Master's in Finance at NUS, the MBA students tended to be civil servants trying to find alternative employment, and more often than not, a local MBA fulfils that objective for them.

Actually, I did hunt for a Masters program in my mid-20s. My GMAT score was 720 with a 6/6 for the essay component - it was enough to get into an MBA program, but probably not the best program on that chart, so instead, I went after the CFA and paid cheap tuition for it - my MSc in Applied Finance cost to be $10k in total. All I paid was the CFA exam and membership fees. I've always been curious what the ROI for my CFA was, given that I never joined the finance industry before Dr Wealth and brought in a 5 figure passive income a month today - would I have the courage to move my funds from unit trusts to manage my own dividend portfolio if I hadn't witnessed how dumb, mathematically inept ( especially those who fail CFA level 2, you know who you are ) and self-serving finance folks can get?

Ok, so now's the hard part, what can we conclude from this data:

a) If you get a local tech or engineering Master, you should seek an overseas posting.

I don't think the situation has changed much for folks who study for a Master's in Computing or Engineering. The range of jobs is not particularly good, so you are better off going off to Silicon Valley and joining a startup that values your skills. I don't think the ROI for a Tech master in Singapore matches the number in the Economist article.

This has not changed for many years; if you are a computing or engineering graduate of any level, you will always be better off working in the United States to build up your experience. The stock options alone might make a millionaire at a very young age.

b) An advanced degree's primary value is in its signalling effect.

I suspect that you are better off signing up for a course I teach at the Polytechnic if you want to pick up actionable and practical skills, I teach Tort Law and Legal Technology, and sometimes I will make you assemble a PDF document using different free software found on the web or employ ChatGPT to analyse a contract. Amazingly, I also teach office politics and how to stop a dagger from being shoved up your back. Also, the course is almost free, thanks to subsidies.

But that's not what most readers of this blog want.

For a Master's degree to have a signalling effect, what is being taught is secondary. Harvard has an excellent case study approach, which makes it the Rolls Royce of MBAs, but the real value of a Harvard MBA comes from the question of who is excluded from the program - which is almost the majority of all applicants. By the time you enter Harvard, you are already a superstar and will build up your social capital working alongside other superstars.

c) Can a bad master's degree tar your resume?You'll only read inconvenient truths on this blog, and I doubt you'll find anything in the mainstream press that will publish stuff like this.

Suppose we believe that some Master's degrees can add a lot of shine to your resume and raise your income. In that case, we have to accept that there is a possibility that some qualifications can reduce your employment outcome even though there's this belief that more learning should be a good thing. After all, we live in a world where a guy can marked down on a dating app if he loves anime or poses with a cat in his profile photo.

For a while, we know the effect being a private university graduate has on your starting salaries. What if having some Masters degrees marks you as having a political orientation or a more hedonistic outlook? It's a stereotype, but some stereotypes are true. In many social sciences, academics are leaning to the far left. Why would a capitalistic and bottom-line oriented multinational company hire them?

Elon Musk tried to hint as such, saying that he prefers skilled tradesmen rather than those incremental political science types - which aligns with the data from The Economist.

d) A Master's degree may be useful in qualification laundering

Sometimes, I get readers stuck in a dead-end job because they have a private degree. In such a case, if they can get a Masters degree from NUS or NTU, it would take the focus away from their private degree when preparing for a job interview. This might be one of the rare and more practical reasons to pick a run-of-the-mill Masters from a local university.

I call this qualifications laundering; it's not a nice name.

But I like it.

Anyway, I'll catch you guys again closer to the new year !